What Is Financial Restructuring of Healthcare and Senior Living?

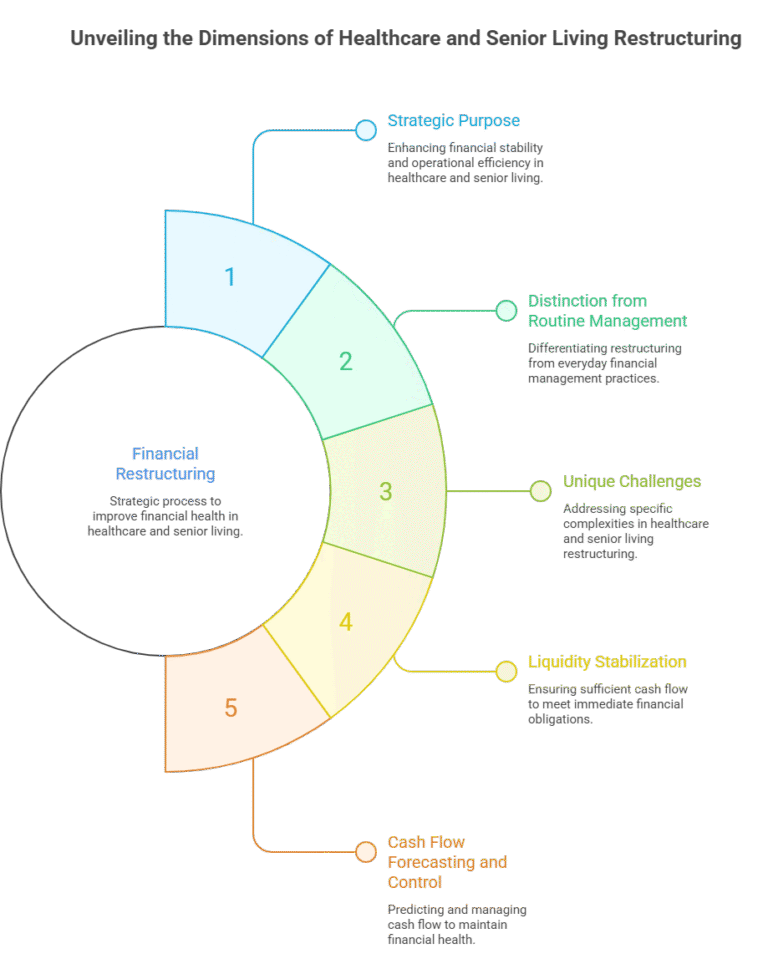

1. Strategic Purpose of Financial Restructuring in Healthcare and Senior Living

2. Difference Between Financial Restructuring and Routine Financial Management

Unlike routine budgeting, accounting, or financial optimization, restructuring is undertaken when an organization is facing material financial distress or heightened risk thereof. This may include recurring operating losses, negative cash flow, loan covenant breaches, declining liquidity ratios, delayed vendor payments, workforce instability, credit downgrades, or inability to fund capital needs. Financial restructuring goes beyond incremental improvement and instead addresses fundamental weaknesses in capital structure, cost base, operating model, and governance.

In every organization, keeping financial activity running smoothly is important. Three terms often used in business finance are routine financial management, turnaround, and financial restructuring, and while they all relate to handling money, they have very different purposes and timing. Routine financial management is the everyday work that keeps a business healthy and on track in normal times. It includes planning budgets, tracking expenses and income, making sure bills are paid on time, managing cash flow, preparing financial reports, and setting financial goals for the future. This is something healthy businesses do all the time to stay organized, make smart decisions, and avoid problems. In simple words, it’s like checking your household budget every month, ensuring you have enough money for bills, savings, and planned expenses. This keeps the business stable but does not involve big changes unless there’s a planned growth or investment need.

A turnaround happens when a business is struggling seriously and needs rapid action to avoid failure. It is usually short-term but intense, with a focus on quickly stopping losses and improving performance. A turnaround may involve identifying why the business is doing poorly — for example, lower sales, rising costs, or poor management decisions — and then taking steps to fix these problems. This could mean cutting unnecessary costs, improving sales strategies, reorganizing teams, prioritizing profitable products, and making urgent operational changes to stop financial decline and start positive growth again. Turnarounds are hands-on and respond to decline by making fast, practical changes to bring the business back into healthier performance.

Financial restructuring, on the other hand, is about changing the way a business is financed when the company has deeper financial stress — especially with how it deals with debt and financing arrangements. Restructuring is most needed when problems are tied to the company’s capital structure — the mix of debt and equity, the schedule of loan repayments, or large borrowings that are hard to manage. In restructuring, a company works with lenders, creditors or investors to adjust its debt agreements, extend payment dates, reduce interest, convert debt to other forms, refinance loans, or even sell non-core assets to strengthen cash reserves. These actions are more formal and strategic than everyday management, and they aim to give the company a new financial foundation so it can survive and operate long-term without constant pressure from heavy debts. Restructuring is like moving from just trying to live within a tight household budget (routine financial management) or trying to stop going deeper into debt (turnaround) to changing how you owe money — such as negotiating with lenders to lower monthly payments or extend the timeline so you won’t be overwhelmed.

To sum up the difference in simple terms: routine financial management is daily financial care for a business in good shape; turnaround is emergency action to stop a decline and quickly improve performance; and financial restructuring is a deeper re-shaping of debt and financing so the business can stand on a healthier financial base for the long term. While all three involve money and planning, they apply at different stages of an organisation’s life — routine management during stability, turnaround during crisis, and restructuring when long-term financial support needs a reset

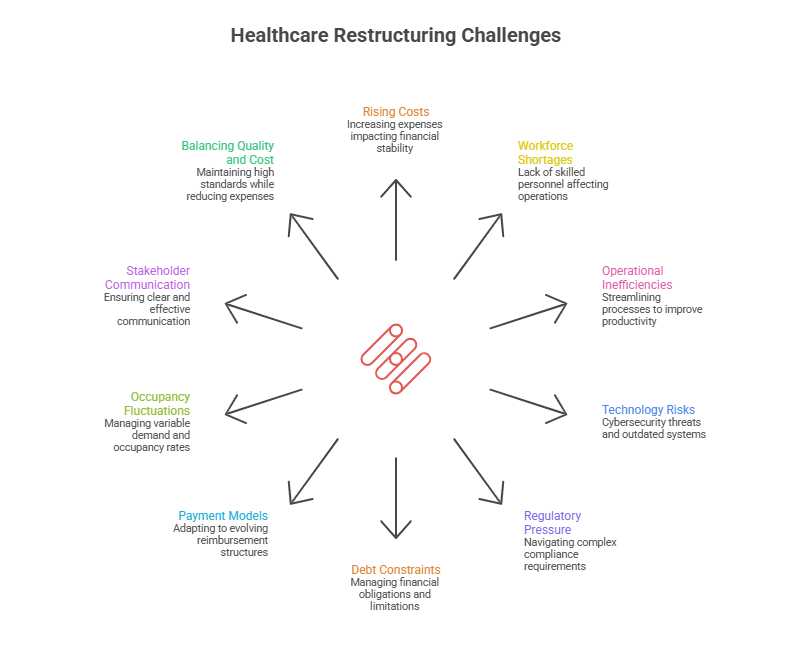

3. Unique Challenges in Healthcare and Senior Living Restructuring

Healthcare and senior living organizations face constant increases in everyday expenses. Labor costs continue to grow due to wage competition and overtime needs. The prices of medical supplies, food services, utilities, insurance, and facility maintenance have also increased significantly. Because many of these costs are fixed or unavoidable, leaders have limited flexibility to reduce spending quickly. During restructuring, controlling these rising expenses while still maintaining safe and effective care becomes a major challenge.

Staffing shortages remain one of the most serious issues in healthcare and senior living. Facilities often struggle to recruit and retain qualified nurses, caregivers, therapists, and support staff. High turnover leads to increased hiring and training costs, and reliance on contract or temporary workers can significantly raise labor expenses. At the same time, fewer staff members can increase burnout and reduce service quality. Restructuring plans must address staffing stability without creating further disruptions.

Many organizations operate with outdated systems, inefficient workflows, and manual processes that slow down productivity. Problems such as billing errors, delayed reimbursements, poor scheduling systems, and weak supply chain management can hurt financial performance. Identifying and correcting these inefficiencies takes time, planning, and sometimes new technology investments. During restructuring, leaders must improve efficiency while managing limited financial resources.

Modern healthcare depends heavily on digital systems such as electronic health records, billing platforms, and communication networks. However, maintaining and upgrading these systems is expensive. In addition, cybersecurity threats continue to grow, and data breaches can result in financial loss and damage to reputation. Organizations undergoing restructuring must protect sensitive information while also deciding how to invest wisely in technology improvements.

Healthcare and senior living providers must follow strict regulations related to patient safety, quality standards, privacy protection, staffing requirements, and reporting. Compliance is not optional, and failing to meet standards can result in penalties, lawsuits, or loss of operating licenses. During restructuring, organizations must ensure that cost-saving efforts do not violate these regulations, which adds complexity to financial decision-making.

Many healthcare and senior living organizations carry significant debt from past expansions, facility upgrades, or operational losses. Loan repayments, interest obligations, and strict lending agreements can limit financial flexibility. Renegotiating terms with lenders or refinancing loans can be a complicated and time-sensitive process. Managing debt while maintaining daily operations is a central challenge during restructuring.

Revenue in healthcare can be unpredictable due to changes in reimbursement structures, insurance contracts, and value-based payment systems. Shifts toward outcome-based payments require investments in quality improvement and reporting systems. Because future income levels may not be guaranteed, financial forecasting becomes difficult, making restructuring plans more complicated.

Senior living communities depend heavily on occupancy levels for stable revenue. When occupancy declines due to competition, economic conditions, or changing consumer preferences, income drops while many costs remain fixed. Attracting new residents often requires marketing efforts, facility upgrades, or service changes, all of which require funding during an already challenging period.

Restructuring can create uncertainty among employees, residents, families, lenders, and community partners. If communication is unclear or delayed, trust can quickly weaken. Employees may fear job loss, and families may worry about quality of care. Leaders must communicate openly and consistently to maintain confidence and reduce disruption.

Perhaps the most sensitive challenge is reducing expenses without negatively affecting patient care or resident well-being. Cutting too deeply in staffing, supplies, or services can harm outcomes and damage reputation. Successful restructuring requires careful decisions that improve financial performance while protecting safety, dignity, and quality standards.

4. Liquidity Stabilization as the First Priority

The foundation of any healthcare or senior living restructuring is liquidity management. Organizations in distress often face immediate cash shortages that threaten payroll, medical supply procurement, and essential services. Restructuring begins with building short-term and rolling cash flow forecasts, often on a weekly or bi-weekly basis, to create visibility into inflows and outflows. This allows leadership to prioritize critical payments, manage working capital, and prevent sudden operational disruptions.

5. Cash Flow Forecasting and Control

Cash flow forecasting in restructuring is not a static exercise but a dynamic management tool. Forecasts incorporate reimbursement timing, payer delays, census or occupancy trends, labor costs, debt service, capital expenditures, and seasonal variability. In senior living, occupancy rates and private-pay collections are critical variables; in healthcare, payer mix and revenue cycle efficiency are central. Accurate forecasting enables scenario planning, lender communication, and decision-making under uncertainty.

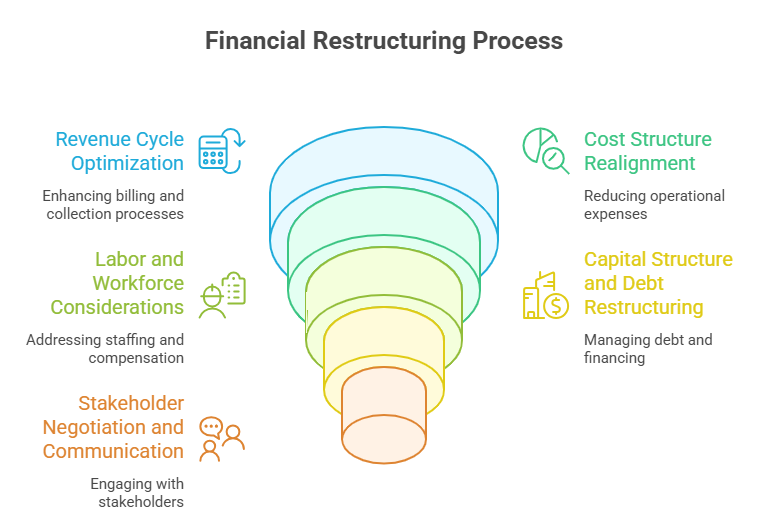

6. Revenue Cycle Optimization

A major component of financial restructuring in healthcare is revenue cycle improvement. Many distressed organizations suffer not from insufficient services but from delayed billing, denied claims, underpayments, and weak collections. Restructuring efforts focus on improving charge capture, coding accuracy, billing timeliness, denial management, and accounts receivable turnover. Strengthening the revenue cycle accelerates cash inflows without compromising care delivery.

7. Cost Structure Realignment

Another critical element of restructuring is cost realignment. Healthcare and senior living organizations often accumulate inefficiencies over time—excess administrative overhead, underutilized facilities, unfavorable vendor contracts, staffing models misaligned with census, and outdated service lines. Restructuring involves detailed cost analysis to distinguish between essential, value-creating expenses and non-essential or inefficient costs. The goal is not indiscriminate cuts but smart cost restructuring that aligns resources with demand and quality standards.

8. Labor and Workforce Considerations

Labor is typically the largest expense in healthcare and senior living. Financial restructuring may involve workforce optimization, but always with sensitivity to care quality, staffing ratios, and regulatory requirements. This can include redesigning staffing models, reducing reliance on agency labor, improving scheduling efficiency, renegotiating labor contracts where possible, and investing in retention strategies to reduce costly turnover.

9. Capital Structure and Debt Restructuring

A defining feature of financial restructuring is capital structure realignment. Many healthcare and senior living organizations carry excessive or poorly structured debt that constrains cash flow. Restructuring may involve renegotiating loan terms, extending maturities, adjusting interest rates, refinancing obligations, or restructuring lease arrangements. In more severe cases, it may include debt-for-equity swaps, asset sales, or recapitalization.

10. Stakeholder Negotiation and Communication

Successful restructuring requires transparent and strategic communication with stakeholders, including lenders, bondholders, landlords, vendors, regulators, boards, and investors. Healthcare restructuring professionals often act as intermediaries, presenting credible financial data, forecasts, and turnaround plans to build confidence and secure stakeholder support. Clear communication helps avoid adversarial outcomes and preserves optionality.

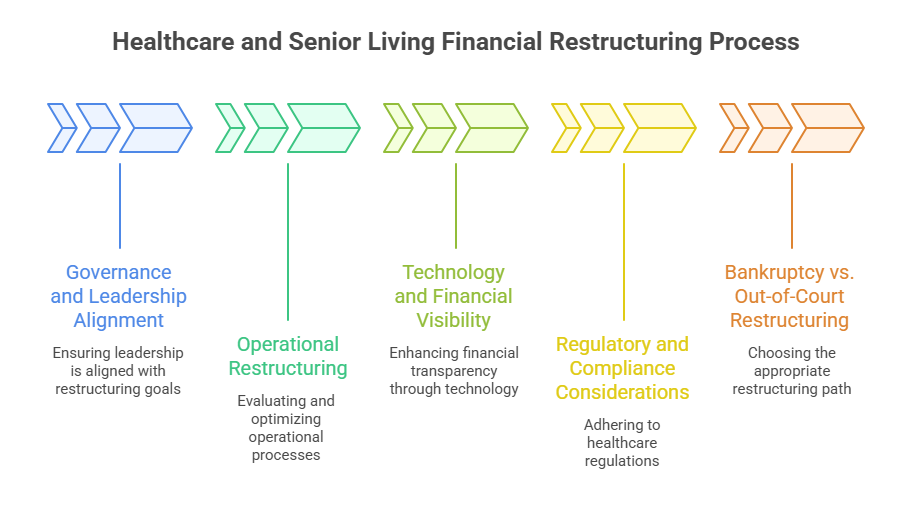

11. Governance and Leadership Alignment

Financial distress often exposes weaknesses in governance and decision-making. Restructuring frequently includes strengthening financial oversight, redefining leadership roles, introducing interim or fractional CFO leadership, and improving board-level financial literacy. Strong governance is essential to ensure disciplined execution of the restructuring plan.

12. Operational Restructuring and Service Line Evaluation

Beyond finances, restructuring may require operational changes. This includes evaluating service lines for profitability and strategic relevance, consolidating underperforming units, optimizing facility utilization, and aligning services with community needs and reimbursement realities. In senior living, this may involve repositioning pricing strategies, care levels, or amenities to improve occupancy and margins.

13. Technology and Financial Visibility

Modern restructuring increasingly leverages technology to enhance financial visibility. This includes improved financial reporting, real-time dashboards, automated reconciliations, and integrated forecasting tools. Better data enables faster decision-making and reduces the risk of future financial blind spots.

14. Regulatory and Compliance Considerations

Any restructuring plan must fully account for healthcare regulations, licensing requirements, payer rules, and quality standards. Financial decisions cannot compromise compliance or patient safety. Restructuring professionals work closely with legal and compliance teams to ensure alignment with regulatory obligations.

15. Bankruptcy vs. Out-of-Court Restructuring

Financial restructuring can occur either outside of bankruptcy or through formal legal processes. Out-of-court restructuring is typically preferred as it preserves control, reduces reputational risk, and minimizes disruption. However, in cases of severe distress, formal restructuring processes may be necessary to reset obligations and protect the organization’s future.

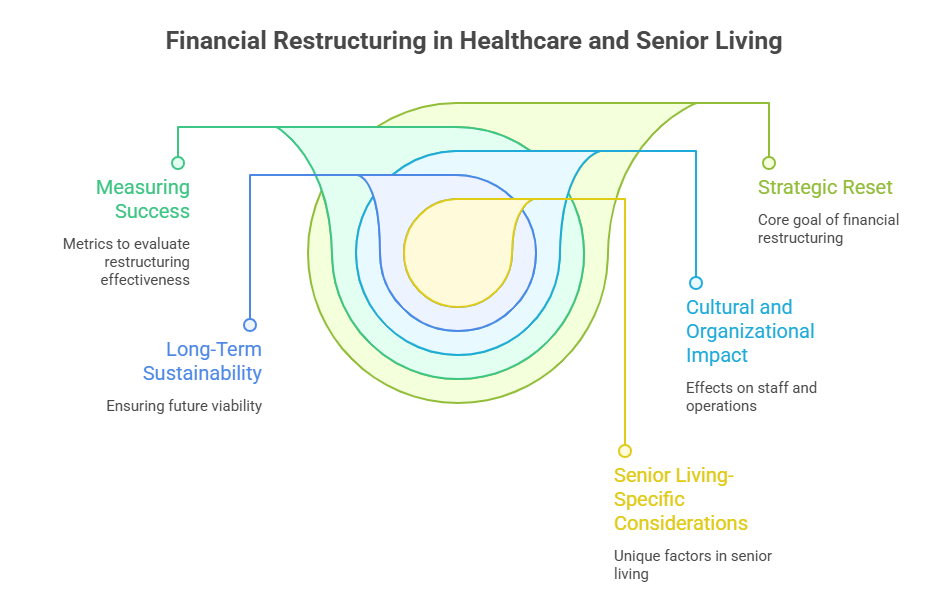

16. Senior Living-Specific Considerations

In senior living, restructuring is heavily influenced by occupancy trends, payer mix (private pay vs. government programs), real estate economics, and staffing availability. Financial restructuring often focuses on improving occupancy, optimizing pricing, controlling labor costs, and aligning services with demographic demand.

17. Long-Term Sustainability and Strategic Repositioning

Restructuring is not complete once liquidity is restored. The final phase focuses on long-term sustainability—developing realistic budgets, strengthening financial discipline, diversifying revenue streams, investing in high-margin services, and building resilience against future shocks.

18. Cultural and Organizational Impact

Financial restructuring also has a human and cultural dimension. Transparency, communication, and leadership credibility are critical to maintaining morale and engagement during change. Successful restructuring builds a culture of accountability, data-driven decision-making, and financial stewardship.

19. Measuring Success of Financial Restructuring

Success is measured not only by improved financial metrics—such as cash flow, margins, and liquidity—but also by operational stability, care quality, staff retention, and stakeholder confidence. A truly successful restructuring leaves the organization stronger than before.

20. Financial Restructuring as a Strategic Reset

Ultimately, financial restructuring in healthcare and senior living is a strategic reset, not a failure. It is a disciplined process that enables organizations to confront financial reality, make tough but necessary decisions, and emerge more resilient, efficient, and capable of fulfilling their mission in a challenging and evolving industry.